Top Market Takeaways Barbie or Oppenheimer – what’s on the market’s big screen?

Market update: Team Barbie or Team Oppenheimer?

The great Barbenheimer debate is rife, and the economy and markets are weighing in. Today, we explore this week’s news flow and offer our thoughts on which side it takes.

1. On the Fed: Despite hiking to levels unseen in 22 years, stocks are having a party in Barbieland.

After over a year of tightening and a “skip” in June, the Fed may be drawing the curtain on its rate hikes. On Wednesday, the Fed hiked 25 basis points to a target policy rate of 5.25–5.5%. Just as expected.

The Fed isn’t taking a victory lap on its fight against inflation just yet, but with a lot of progress so far (at the same time the economy has stayed on solid footing), we think it’s probably the last hike of the cycle (or close to it). It could also be the start of the end of an era – the European Central Bank signaled it could be wrapping up hikes this week, and the Bank of Japan surprised by widening its yield curve control policy overnight.

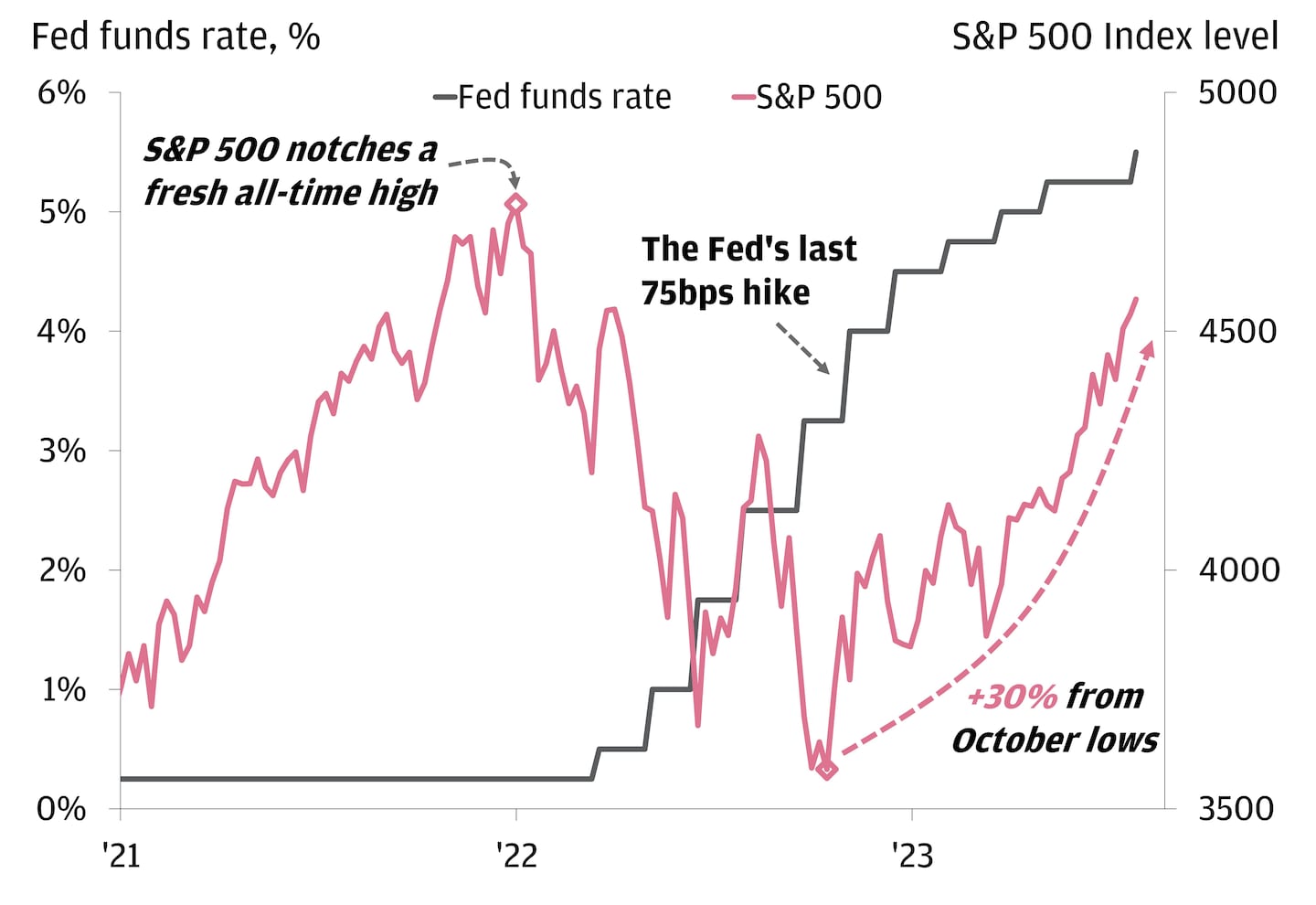

Whether the Fed ultimately gets a reputation for achieving a soft landing or spurring a mild recession, stocks have moved on from the debate. After a rough 2022 as the Fed got going, the S&P 500 is now up some 20% this year and is less than 5% off of last January’s record highs. It’s also likely not a huge coincidence that the market bottomed around the same time the Fed delivered its final monster 75-basis-point hike (marking a slower pace from there).

Stocks seem to have moved on from rate hikes

2. On the economy: Even the recessionistas can’t deny the recent Barbie vibes

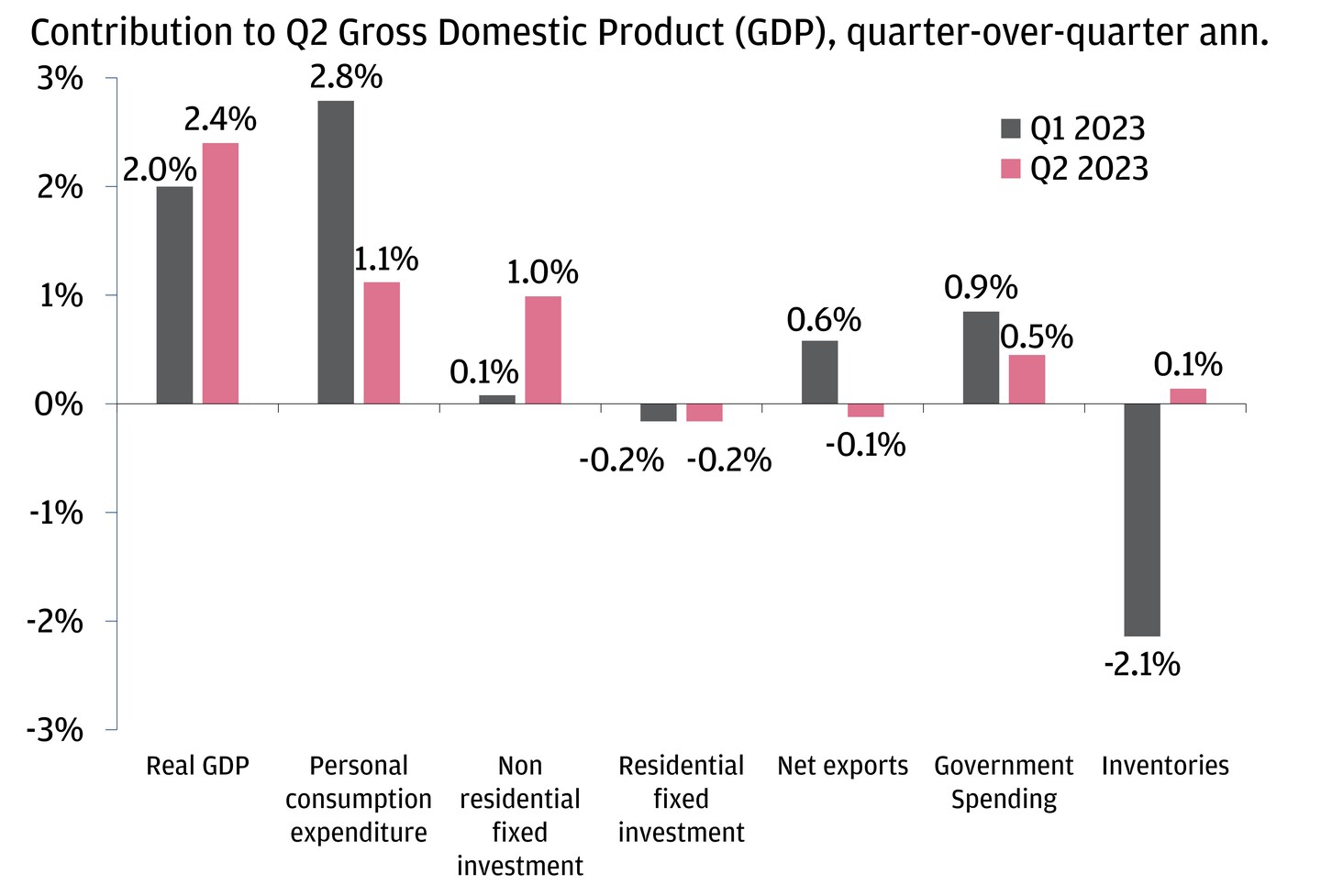

The U.S. economy is still feeling good. Yesterday brought the official read on growth in the second quarter, with GDP printing at an above-expected 2.4%. The sources of the boost added to the flare – consumption saw a solid lift (from spending on both goods and services), prices cooled and capital expenditures spending popped thanks to industrial policies like the Inflation Reduction Act.

Q2 GDP showed the U.S. economy is in the summer mood

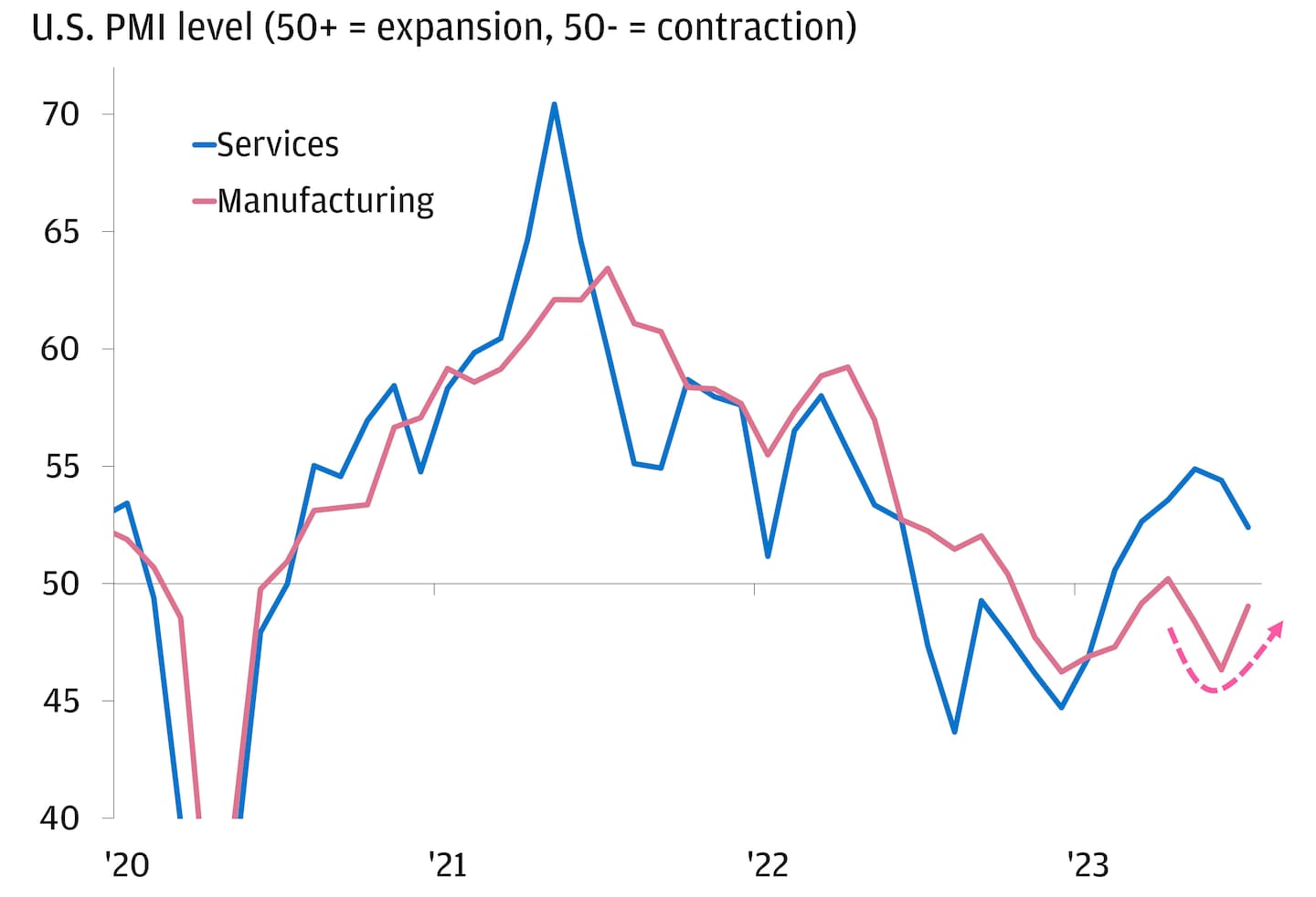

Other measures sang to the same tune. The number of Americans that applied for unemployment benefits in the last week hit its lowest since February. And in a sign that last year’s downtrodden sectors may be finding their footing, a key leading indicator for manufacturing saw its first increase in three months as contracts to buy previously owned homes climbed.

Reshuffle: U.S. manufacturing could be finding its footing

Meanwhile, Europe is having a bit of a more Oppenheimer summer. Manufacturing activity worsened even more in June, services parts of the economy are now seeing softer momentum and business sentiment is also taking a hit (just look to Germany’s latest IFO reading). The upshot, though, is that inflation is also cooling – the bad news comes with some good.

3. On earnings: Oppenheimer may get this quarter, but Barbie is still working some magic.

This week marks the busiest for Q2 earnings.

The not-so-good news: So far, it’s shaping up to be the worst quarter since Q2 2020 (with consensus anticipating earnings to contract -7.5% year-over-year). While almost 82% of the companies that have reported have beaten estimates (handily above the 77% average over the last 5 years), they’re “only” beating at a rate of 6.5% (compared to the 8.4% 5-year average). That feels Oppenheimer-y.

But we also see some Barbie vibes. It could be the case that the bar was set pretty high heading into the season. That’s meant that names that have had a good run (like Microsoft, Netflix, Tesla or LVMH) are being punished for results that, to us, don’t look all that bad (or far from it). When you look under the hood, it’s still shaping up to be a decent season – even a good one – for many bellwether companies. Banks have done much better than expected (not to mention the PacWest and Banc of California merger was also good news for the sector this week), some other mega cap tech names are going from strength to strength, and a handful of consumer companies are showcasing still-robust spending.

4. On commercial real estate: Oppenheimer in the office space, but less gloomy as a whole.

CRE, especially in the office space, has been feared as one of the biggest ripple effects of the bank crisis.

The Oppenheimer crew might lean on climbing vacancy rates in big cities. Look no further than the latest cover1 of New York magazine. According to researchers2 from Harvard and MIT, there’s around 75 million square feet of vacant office space in New York City – enough to fill more than 26 Empire State Buildings!

And that stretches beyond just the Big Apple. Jones Lang LaSalle Inc. (JLL) recently noted that less than 5 million square feet of new offices have broken ground this year, while 14.7 million square feet have been axed – that’s the first net decline since at least 2000. This lack of income puts loans issued by banks for CRE at risk – but it’s still TBD what the correction will look like.

The Barbie folk might argue that the office sector represents such a small part of the overall economy (office construction remains a modest 0.4% of U.S. GDP), and that challenges here can’t be generalized. There’s certainly weight to that, but the risk of CRE loans to small banks probably gives this round to the Oppenheimer's for now.

5. On China: Policymakers are doing the Barbie song and dance, but growth has yet to get its heels back up.

Earlier this week, China’s Politburo (its top decision-making body) called for adding more support for the property sector (which continues to weigh on growth), improving domestic demand (to boost incomes and consumption in areas like travel, leisure and sports), and strengthening “counter-cyclical” adjustments.

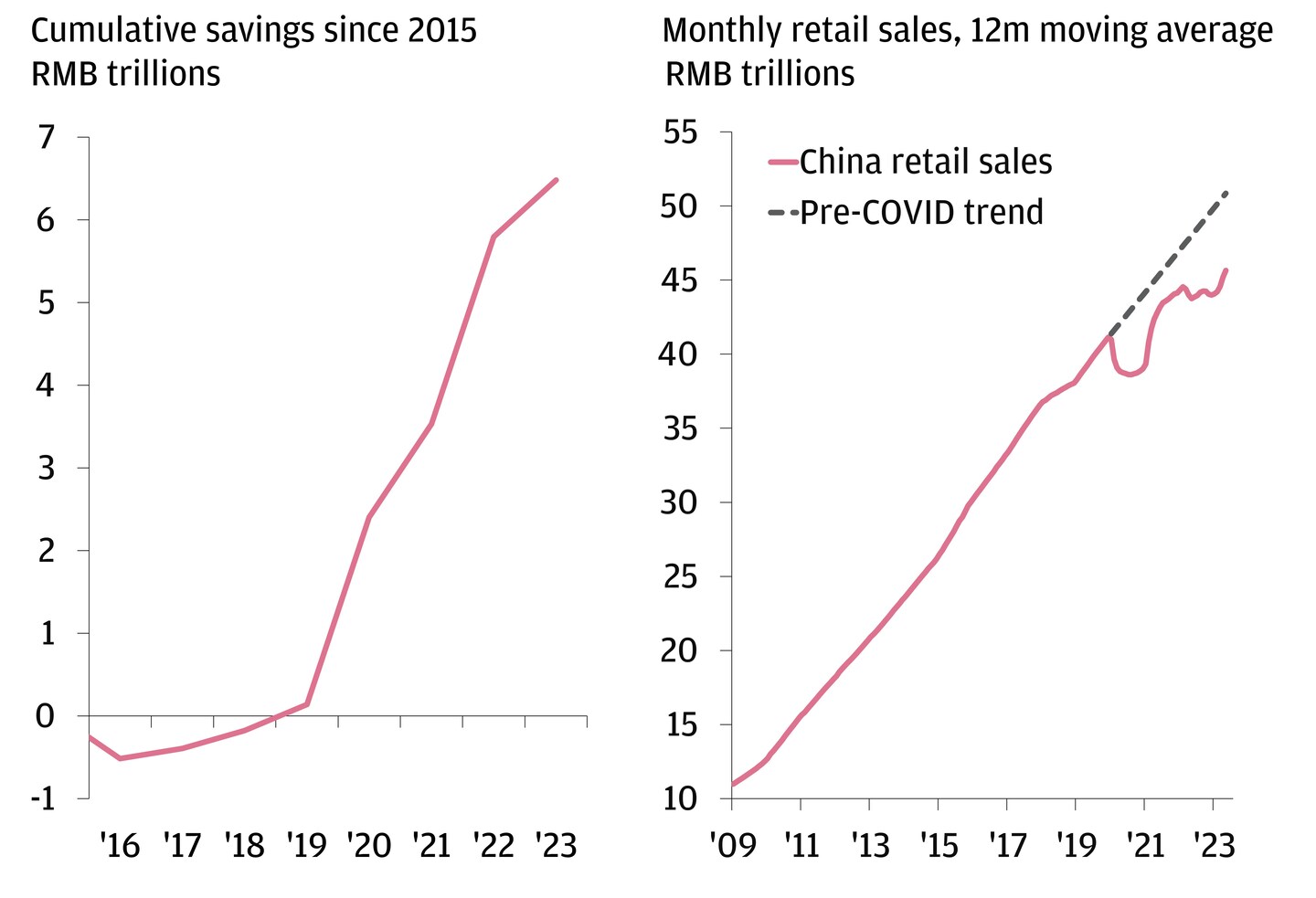

The feel is that while it’s still China’s same brand of “mini easing,” the tone was more pro-growth and constructive than it has been. At some point, all the slow-moving stimulus could help move the needle, and get the consumer going. There’s still much progress to be made: Chinese consumers are sitting on hordes of excess savings, and retail sales are still 10% below their pre-COVID trend.

A catch-up play by the Chinese consumer could support growth

With all that in mind, the Hang Seng rounded out this week with a +4.7% gain.

And the winner is….

Both Barbie and Oppenheimer have blown past box office expectations, sending cinema stocks like AMC, IMAX and Cineworld soaring on Monday. Yet, it was Barbie that almost doubled Oppenheimer’s total sales during its opening weekend. While it’s yet to be seen if its hold remains, stocks at least seem to agree with the winner, and have continued their summer vibe-shift.

While it may not be all smooth sailing, the rally offers an opportunity to broaden and balance equity portfolios (into undervalued pockets of the market like mid-caps, dividend-growth companies and long-term trends around the energy transition, industrial policy and digital transformation). The recent pop in yields (10-year Treasury yields climbed back above 4% this week) offers a still-compelling entry point in fixed income. And with borrowers turning to alternative sources of lending as banks tighten their standards, now could be the time to take advantage of private credit and stressed/distressed opportunities.

Your J.P. Morgan team is here to discuss these dynamics, and maybe even offer their take on which flick they liked better.

All market data from FactSet and Bloomberg Finance L.P., 7/28/23.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Footnotes

-

1

New York Magazine, “New Glut City: The city’s mega-office landlords are panicking, pivoting, and shedding what’s worthless. One opens his books.” (July 2023)

-

2

New York Times, “26 Empire State buildings could fit into New York’s empty office space. That’s a sign.” (May 2023)